Main Street America recently conducted a follow-up to its survey on the impacts of COVID-19 on small businesses to better understand the continued challenges businesses face as the crisis evolves. The hundreds of responses we received from business owners across the country indicate that small businesses remain severely challenged by reduced revenues and are uncertain about their path forward. Federal financial programs associated with COVID-19 have provided stopgap support but may ultimately offer limited relief as the public health crisis looms large in the minds of consumers.

Detailed findings are outlined below, followed by recommendations for Main Street programs to consider as they begin the recovery process.

Findings

Less than half of respondents who applied for federal relief dollars in the initial stimulus round received funding, and the smallest businesses had the least success with their applications. As of the end of the first federal funding allocation, 78 percent of the small businesses who responded to the follow-up survey had applied for federal relief associated with COVID-19. Of those who applied, 48 percent received funding. The smallest businesses responding to the survey had the least success with their applications: Of those business owners who applied and have fewer than 6 employees, 39 percent received funding. In comparison, 64 percent of business owners who applied and have six or more employees received funding.

Businesses in small towns applied for federal relief dollars less often and had less success receiving funding. As of April 23rd, businesses from larger towns and cities—places with at least 50,000 residents—had applied for federal relief in greater proportions and received funding in greater proportions. In our sample, 89 percent of businesses in larger towns and cities applied for federal relief, compared to 76 percent of businesses in places with fewer than 50,000 residents. In the smallest towns—places with fewer than 5,000 residents, only 69 percent of businesses in our sample applied for federal relief dollars. 59 percent of those who applied from places with 50,000 residents or more received funding, compared to 45 percent of those who applied from places with fewer than 50,000 residents.

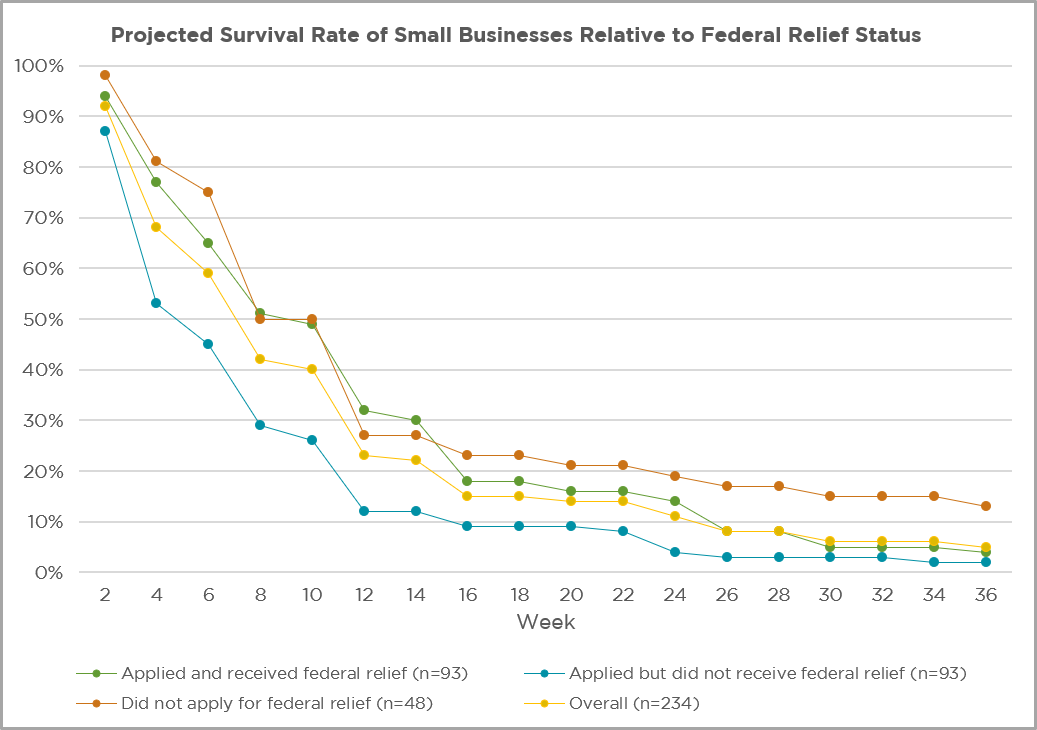

Funding from the Payroll Protection Program (PPP) and Emergency Injury Disaster Loan (EIDL) offered little long-term financial relief. Half of the businesses that received funding through the PPP or EIDL programs and disclosed their funding amount received less than $8,000, suggesting that those businesses had relatively few employees and limited payroll expenses. Separately, we asked business owners how long their businesses could avoid permanent closure if current trends continue, and 234 businesses provided an estimated number of weeks they could stay open. Of those, 93 businesses had applied for PPP or EIDL funds and received money, 93 had applied and not received money, and 48 had not applied for either program. The businesses who had received PPP or EIDL funds provided an average estimated life expectancy of 12 weeks and 6 days, which is about 30 days longer than the average estimated life expectancy of businesses who applied but did not receive federal relief.

More than a third of businesses earned no revenue in April and laid off or furloughed their entire staffs. Personal care businesses were hit especially hard. 34 percent of businesses in our sample generated no revenue in April, and 35 percent had laid off or furloughed their entire staffs. Personal care businesses, including salons, nail salons, and barbershops, were especially impacted. 73 percent of personal care businesses in our sample did not earn revenue in the month of April, and 76 percent had laid off or furloughed their entire staffs. Food service businesses and non-food retail establishments were also hit hard: More than a quarter of food service businesses (31 percent) and non-food retail (28 percent) businesses generated no revenue in April. Across all 631 businesses represented in both the original and follow-up surveys, 2,246 employees had been laid off or furloughed--an average of 3.5 employees per business in our sample.

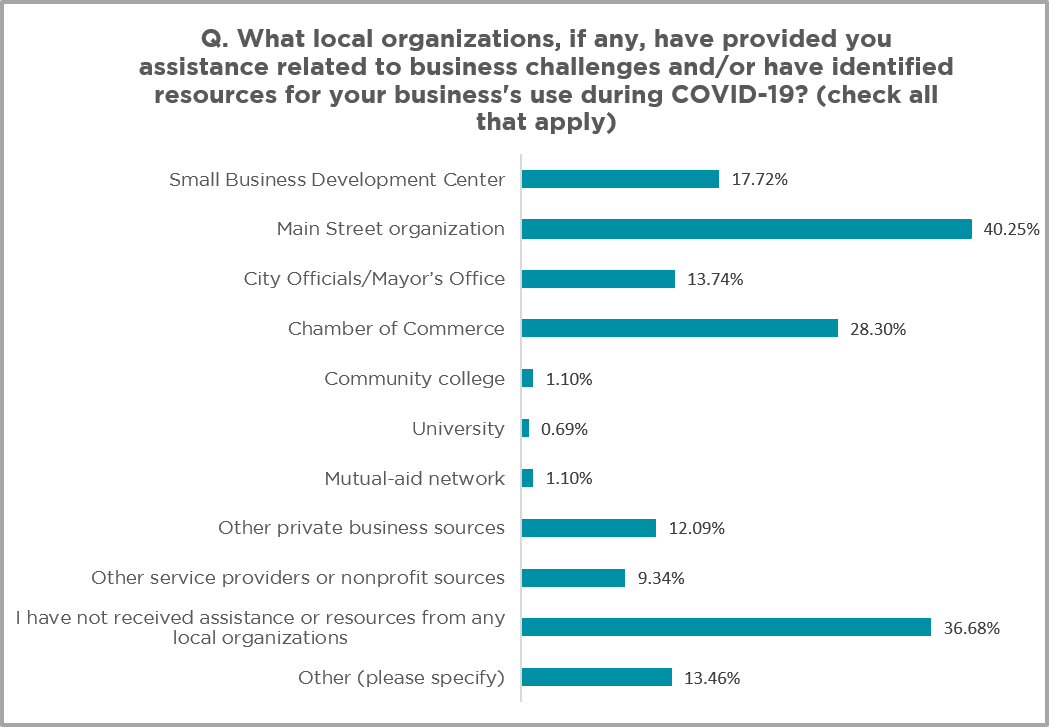

Local Main Street programs play a critical role in supporting small businesses across America. Main Street programs were a key provider of assistance to small businesses responding to our survey. Of the complete set of 728 small business respondents, 40 percent of businesses said that they’d received assistance from their local Main Street organization. More than 2.25 times the number of respondents indicated they’d gotten support from Main Street than support from any other source, aside from Chambers of Commerce, and Main Street was identified as a recent source of support by 42 percent more businesses than even Chambers of Commerce.

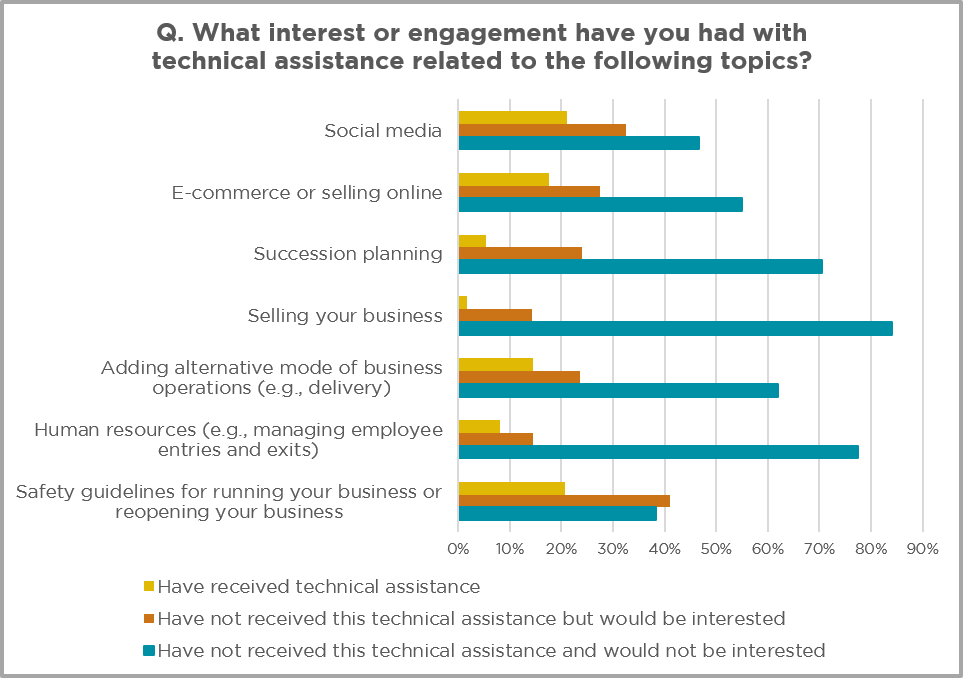

Business owners are most interested in technical assistance focused on operating their business safely. We asked small business owners about their prior experience and future interest in seven types of technical assistance. Of the seven types, only one type—“Safety guidelines for running your business or reopening your business after a temporary closure”—elicited more interest than disinterest among the complete sample of 728 respondents. For that option, 41 percent of respondents said they hadn’t received that kind of technical assistance but would be interested, 38 percent said they hadn’t received it and weren’t interested, and 21 percent said they had already received such technical assistance.

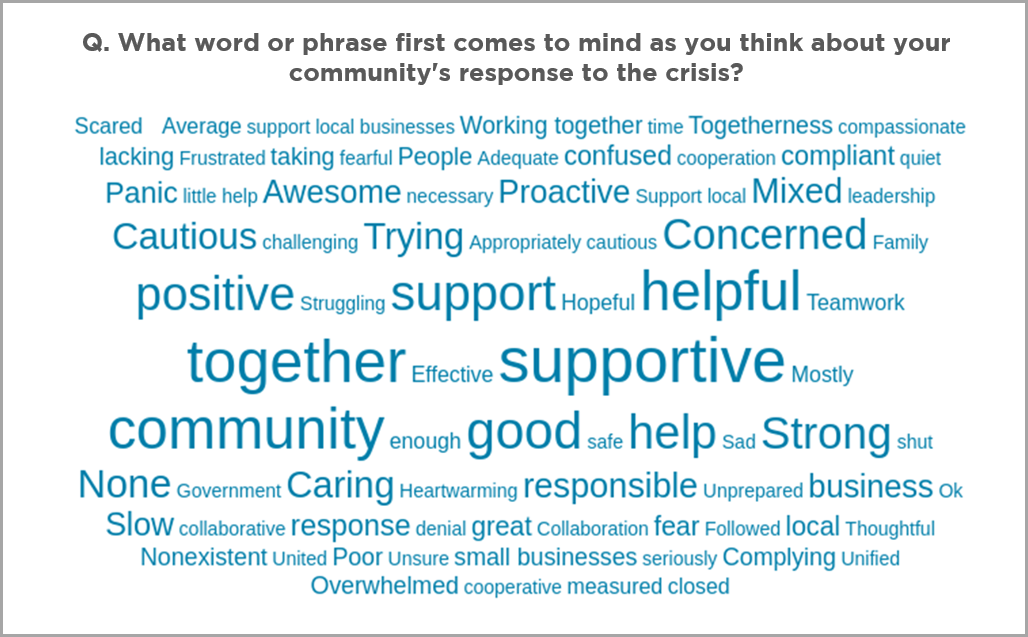

Communities are working together and supporting small businesses through the crisis. As one of the final questions on the follow-up survey, we asked business owners what word or phrase came to mind as they think about their community’s response to the crisis. This was a purely open-ended question, but some clear trends emerged in the complete set of 728 responses. 14 percent of respondents wrote in words like “supportive,” “support,” “helpful,” or “help.” 8 percent of respondents wrote words like “together,” “working together,” “togetherness,” or “community.”

What this means for local Main Street programs

As we analyze the survey results, there are a few recommendations for Main Street programs to consider as you help small businesses in your community recover and as you evaluate and address your own organization’s well-being.

1. Small businesses are turning to Main Street programs more than any other service provider for both technical assistance and as a connector to important survival resources. The latest survey reveals that Main Street programs provided assistance to 40 percent of the respondents when they sought support with business challenges or identifying financial resources. In comparison, 28 percent received assistance from Chambers of Commerce, 18 percent from Small Business Development Centers, and 14 percent from city government officials.

As financial support for local community and economic development organizations becomes more competitive and limited from funders like cities, states, and businesses, positioning your Main Street program as a critical connector and educational resource for small businesses will be a key message when advocating for continued and new financial support. Use the results of this survey in conjunction with a short-term (recommend 90 days) Recovery Plan to help build your advocacy campaign for implementation resources that will be needed beyond a reopen proclamation.

2. As we compare the results from the first national Main Street America survey to the findings from this survey, it is clear that business needs will be evolving quickly as we move from crisis to recovery. As such, when examining business needs, which range from guidance on safety guidelines to e-commerce, Main Street programs will need to be agile in their ability to acquire technical assistance resources for their small business owners. Please note that the new Main Street Forward resource center has a section agglomerating safety guideline examples for various retail sectors that can be shared with local small businesses.

Secondly, Main Streets should be flexible as they develop grant and/or loan resources to aid in the recovery, as needs will be much more nuanced and thus not suited for a one-size-fits-all solution. For example, while it’s clear based on survey data that many small businesses need e-commerce capabilities, designing a program exclusively for e-commerce, while important, may exclude many business owners who need other forms of technical and financial assistance.

We encourage programs to first evaluate, through a series of business interviews, business model shifts resulting from the pandemic. Then, create flexible “business model grants” that help small business owners execute on plans to address a variety of market shifts. For example, these grants could help a restaurant with interior renovation needs to host cooking classes or provide a women’s apparel store with the capital needed to add a casual wear clothing line so that they can cater to those now working from home.

Finally, work with your local/regional Small Business Development Centers. As part of the CARES Act funding, SBDCs received additional resources that can be used to sponsor expanded educational and counseling services that you identify as needs in your districts.

3. While there is much uncertainty in the world due to the pandemic, what is very apparent is that reopen proclamations don’t mean a return to pre-COVID-19 norms. This is a moment when we cannot simply turn the light switch back and expect a return to normal. Businesses will still be healing from weeks and weeks of limited to no revenues. Consumers will still be impacted from potential unemployment worries, feel a need to conserve their financial resources, and have concerns around shopping safety measures.

As such, the programs and activities that you were running during stay-at-home orders from crowdfunding programs for small businesses to virtual retail promotions and reclaimed streets for delivery and pick-up should remain in place. Furthermore, consider potentially expanding those elements or tweaking, as needed, to allow for a more hybrid recovery approach that takes into account changed shopping norms. For example, as restaurants reopen, continue to evaluate reclaiming streets for not only delivery and pick-up, but also leveraging additional parking spaces for outdoor dining spaces to account for social distancing needs.

As businesses evaluate their operating models, technical and financial needs, and how to best position their stores in a recovering economy, Main Street organizations will need to be doing the same thing. This second round of survey results are part of the Main Street Forward recovery-oriented resource center. In addition to Main Street America’s research activities, you will find valuable recovery planning tools, network best practices and examples, along with guidance on Four Point related activities to help guide you through these very challenging times.

METHODS

This survey was conducted between April 24 to May 4 as a follow-up to our initial national survey conducted between March 25 and April 6 focused on the impacts of COVID-19 on small businesses. The survey was distributed using SurveyMonkey to small businesses who opted in during the initial round. Questions on our follow-up survey focused on financial relief and other forms of support offered to small businesses, recent impacts of COVID-19 on business revenue and staffing, characteristics of their business location, and community-level responses to the COVID-19 crisis.

We received 728 complete follow-up surveys, and we were able to join 631 of those surveys to responses on our original survey round. Nearly 100 new email addresses were used in the follow-up survey and it is unclear if those email addresses were secondary email addresses from participants or if new participants joined in. In the analysis used here, we worked from the sample of 631 responses where we had two complete surveys unless noted.

As with our original survey, about 40 percent of respondents in our follow-up survey own businesses in towns with fewer than 10,000 people. Only six percent came from cities with 50,000 – 99,999 residents, and six percent came from cities with more than 100,000 residents. Follow-up surveys came from 43 states and the District of Columbia, with Pennsylvania (n=74), Indiana (n=46), and Washington (n=31) most represented. 94 percent of businesses respondents have fewer than 20 employees. 69 percent have fewer than six employees. 76 percent of the business respondents are locally owned, and 61 percent are woman owned. As with our original survey, close to half of the respondents owned businesses that had been in operation for over ten years.

Disclaimer: This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for legal, insurance, liability, tax, or accounting advice. You should consult your own legal, insurance, tax, and accounting advisors for guidance on these matters.